My Business Consulting DMCC is an independent management consulting firm, providing advisory and administrative support for company formation, immigration, banking, and related services in the UAE. We are not a government authority; all official documents and approvals are issued exclusively by the respective government entities.

VAT in UAE Designated Zones

Thinking about opening an import/export business in the UAE? Designated Zones allow you to save in many areas including taxes. Foreign investors usually go through very minimal documentation and straight forward registration process.

What are Designated Zones in the UAE?

A Designated Zone is any specific area assigned by Cabinet Decision to be outside the UAE for Value Added Tax (VAT) purposes. Territories designated to offer incentives to businesses. For this to happen, a number of conditions need to be fulfilled.

Ras Al Khaimah

RAK Free Trade Zone

RAK Maritime City Free Zone

RAK Airport Free Zone

Abu Dhabi

Free Trade Zone of Khalifa Port

Abu Dhabi Airport Free Zone

Khalifa Industrial Zone

Sharjah

Hamriyah Free Zone

Sharjah Airport International Free Zone

Fujairah

Fujairah Free Zone

Fujairah Oil Industry Zone (FOIZ)

Dubai

Jebel Ali Free Zone

Dubai Cars and Automotive Zone (DUCAMZ)

Dubai Textile City

Free Zone Area in Al Quoz

Free Zone Area in Al Qusais

Dubai Aviation City

Dubai Airport Free Zone

Umm Al Quwain

Umm Al Quwain Free Trade Zone in Ahmed Bin Rashid Port

Umm Al Quwain Free Trade Zone on Sheikh Mohammed bin Zayed Road

Ajman

Ajman Free Zone

IMPORTANT: Sale or Lease of Commercial or Residential Property located in any of the UAE Designated Zones is out of scope of VAT

Sale and/or lease of commercial and residential properties within UAE Designated Zones will be out of scope of VAT, according to the latest clarification issued by the Federal Tax Authority (FTA).

“Sale or lease of any real estate property – commercial or residential – will be considered as outside the scope of VAT. Hence, there will be no VAT applicable on sale or lease of commercial or residential real estate properties in designated zones.”

Cabinet Decision No. (59) of 2017 on Designated Zones for the purposes of the Federal Decree-Law No. (8) of 2017 on Value Added Tax, effective Jan 1, 2018.

How is VAT applicable in UAE Designated Zones for Commercial Businesses?

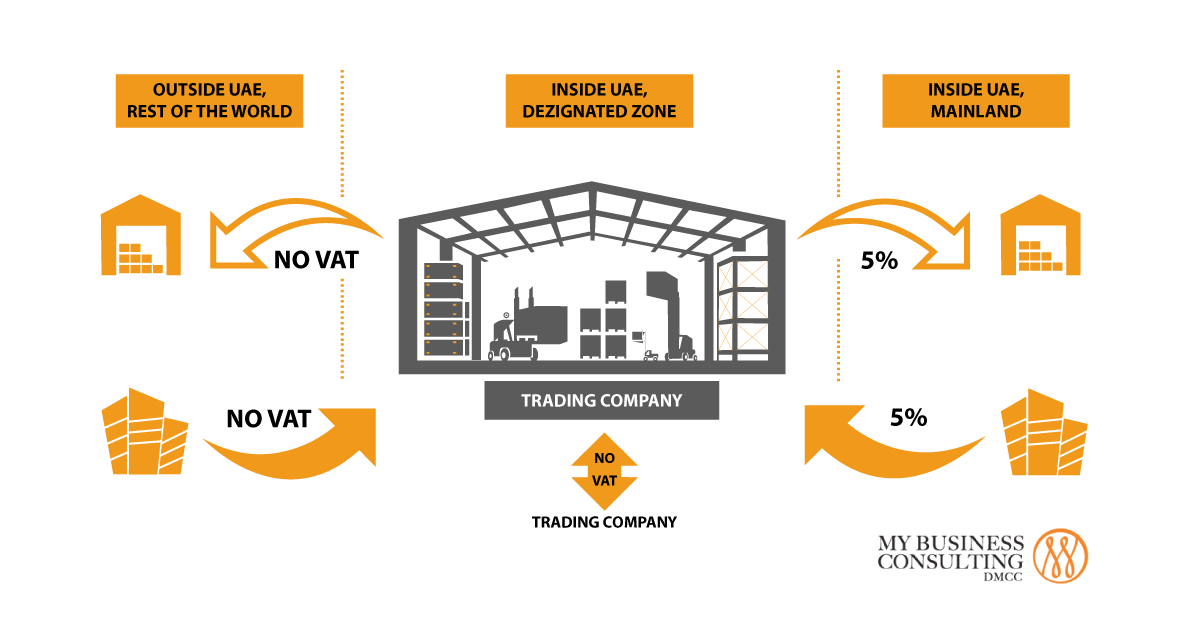

Even if Designated Zones are located inside the territory of the UAE, for VAT purposes, they are dealt with as being outside the UAE for trading with goods.

A. Supply of Goods from and to the Rest of the World (out of the UAE).

VAT is not applicable for sales and purchase of goods within or between UAE Designated Zones until these goods are exported or used to manufacture taxable supplies.

Example: Company A has purchased fruits from Company B (both companies are located in UAE Designated Zones). Company B produced jam out of these fruits. In case Company B decides to sell it to UAE Mainland the Company B will bear 5% VAT from the first transaction (purchase of fruits) and charge accordingly VAT on sale to Company or Individual located in Mainland. However, if Company B exports the jam to ROW (Rest of the World), VAT is not applicable neither on purchase or sale of fruits/jam.

B. Supply of Goods Between Designated Zones in the UAE.

Supplies between the Designated Zones is out of scope of VAT, provided that:

The Goods are not released during transfer between the Designated Zones

Goods are not in any way used or altered during the transfer between the Designated Zones.

The transfer of goods is undertaken in accordance with the rules for customs suspension according to GCC Common Customs Law.

The owner of goods provides a monetary guarantee to the authority, if the conditions for movement of goods are not met.

C. Supply of Goods from and into UAE Mainland

5% VAT is applicable in both cases

How is VAT applicable in UAE Designated Zones for Service Businesses?

Service is anything that can be supplied other than Goods. The Executive Regulation specifies that the place of supply of services is considered to be within the UAE if the place of supply is within the Designated Zone. This indicates, any services whether supplied from the mainland to Designated Zone or within the Designated Zone, the standard rate of VAT at 5% will be imposed.

*Reverse Charge Mechanism (RCM) – when the obligation to pay tax is applicable on the beneficiary of the supply rather than the supplier. When the Reverse Charge is applied, the beneficiary of the goods or services makes the declaration of purchase (input VAT) and the supplier’s sale (output VAT) in their VAT return. That is how both entries cancel each other (5% PLUS and 5% MINUS).

VAT treatment for supply of goods and services related to Designated Zones are different. Tax free transactions are available only for the supply of goods within the Designated Zones, provided that conditions, as prescribed in UAE Executive Regulations are met. Therefore, for UAE businesses, it is certainly important to understand VAT treatment on supplies carried out by them, assess the impact of VAT on their business and accordingly apply.

My Business Consulting has over 18 years expertise in Tax Advisory, Accounting and Bookkeeping. We can help your business enjoy huge tax and business benefits offered by UAE Designated Zones. We understand the UAE foreign investment terrain, tax regime and accounting system very well.

Shall you require a customized VAT Consultation or an in-depth VAT Training to learn how to apply VAT for your business model – call us today.

Each one of the UAE Designated Zone offers wonderful schemes for foreign investors but they’re not all the same. To start business in these hugely beneficial Designated Zones, new investors particularly may get in touch with My Business Consulting to access the latest information on available facilities and to help them settle perfectly in UAE Designated Zones.